Americans hold more money in Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) each year—a trend that represents a major opportunity for ecommerce brands and omnichannel retailers. By accepting payments from these accounts, retailers tap $150 billion in spending power while increasing cart size by up to 30%.

But HSAs and FSAs are heavily regulated by the IRS, and all purchases must qualify as eligible medical expenses. Retailers play a major role in this compliance ecosystem. In fact, the IRS mandates that most businesses adopt a special inventory system (called IIAS) to help “substantiate” legitimate HSA/FSA purchases.

Below, we’ll provide detailed instructions on how to meet HSA/FSA requirements—and explain the advantages of using a dedicated HSA/FSA payment provider to maintain compliance while boosting sales.

Understanding HSAs, FSAs, and HRAs

HSAs and FSAs, as well as a similar tool called a Health Reimbursement Arrangement (HRA), provide consumers with tax benefits for money that’s been set aside for medical expenses.

Here’s a breakdown of these accounts:

- A Health Savings Account (HSA) is a special type of savings account that allows consumers to set aside untaxed funds to be used for qualifying medical expenses.

- A Flexible Spending Account (FSA) is an untaxed account, often funded by an employer, that can be tapped for medical expenses.

- A Health Reimbursement Account is an employer-funded health plan that allows employees to be reimbursed for medical expenses.

These accounts are growing in popularity. Between 2017 and 2022, the number of HSA accounts increased by more than 60%—and as of 2024, more than 61 million Americans were covered by one.

For ecommerce brands and omnichannel retailers, this trend represents a major opportunity to raise average order values (AOVs) while increasing customer loyalty.

The Complexities of IRS Substantiation

To ensure compliance with IRS guidelines, retailers must confirm that each HSA/FSA purchase falls within the IRS’s definition of a “medical expense.” The IRS verifies the eligibility of these purchases through a process called “substantiation.”

The IRS Definition of “Medical Expense”

In Publication 502, the IRS defines medical expenses as “the costs of diagnosis, cure, mitigation, treatment, or prevention of disease, and for the purpose of affecting any part or function of the body.” This can include “legal medical services rendered by physicians, surgeons, dentists, and other medical practitioners” as well as “the costs of equipment, supplies, and diagnostic devices.”

Examples of Qualifying Medical Expenses

The IRS has provided a detailed list of items and services that are eligible for purchase with HSA/FSA funds. Some of these products and services include:

- Braces

- Contact lenses

- Chiroporactors

- Drug addiction therapy

- Eyeglasses

- Prescription medications

- Equipment for the hard-of-hearing

- Therapy equipment

- and much more…

The list provided by the IRS should not be considered exhaustive. Additional products and services can be purchased with HSA/FSA funds as long as the customer shows evidence of genuine medical necessity.

Additional Eligible Expenses

In addition to the medical expenses explicitly mentioned by the IRS, customers can use HSA/FSA funds for “dual-purpose” products and services that serve a genuine medical need. To use HSA/FSA funds for these purchases, customers must acquire a Letter of Medical Necessity (LMN) from a qualified physician.

An LMN is a specific kind of doctor’s note explaining why a patient requires a certain product or service for medical reasons. LMNs are increasingly easy to access thanks to the rise of telehealth, with many retailers even incorporating telehealth LMNs into the checkout process.

The Need for Third-Party Substantiation

To remain compliant with IRS regulations, purchases made with HSA/FSA funds must be substantiated by a third party. In IRS Memorandum 202317020, Laura Warshawsky explains that an FSA is not compliant if it “does not require an independent third party to fully substantiate reimbursements for medical expenses.”

In many cases, "auto substantiation" simplifies the process for consumers. There are 3 main methods for obtaining third-party auto substantiation for medical expenses:

- Real-time substantiation. When the customer purchases an eligible product or service through a retailer that utilizes an Inventory Information Approval System (IIAS), the substantiation should occur immediately and automatically.

- Copayment match substantiation. This applies if the copayment for an eligible medical expense matches the transaction amount shown in an HSA/FSA account.

- Recurring claims substantiation. If a consumer consistently pays the same dollar amount to a single provider and successfully substantiates the first claim, subsequent claims will be automatically substantiated.

When auto substantiation isn’t possible, customers will have to submit substantiation documentation themselves. This documentation should include:

- The customer/patient’s name

- The provider/merchant’s name

- The provider/merchant’s address

- The date of the service or expense

- A detailed description of the expense or service

- The amount charged

Regardless of whether an expense is auto-substantiated, customers should always save an itemized receipt when using HSA/FSA funds.

Common Compliance Pitfalls

In an effort to expedite the substantiation process, merchants and consumers sometimes fall short of maintaining compliance.

Here are some examples of common “shortcuts” that the IRS declared impermissible in Memorandum 202317020:

- Self-certification. The customer can’t attest to the medical necessity of a purchase without the backing of a third party.

- “Sampling.” Third parties can’t substantiate just some of a customer’s HSA/FSA-funded purchases. Each expense must be substantiated individually.

- Favored providers. Customers must receive third-party substantiation for all expenses, including those incurred with medical providers. Showing receipts only from non-healthcare providers isn’t enough.

- De minimis. It is not sufficient for customers to provide substantiation only for purchases above a certain dollar amount. All purchases, regardless of their size, must be accompanied by third-party substantiation.

- Advance substantiation. Customers cannot substantiate purchases to be made in the future.

The Consumer’s Role in Maintaining Compliance

Customers, too, play a crucial role by retaining accurate records such as receipts or Letters of Medical Necessity (LMNs), typically for three to seven years. As the IRS states in Publication 969, “You must keep records sufficient to show that the distributions were exclusively to pay or reimburse qualified medical expenses.”

Auto-Substantiation & IIAS Systems

Auto substantiation allows merchants and consumers to overcome the challenges of traditional HSA/FSA substantiation. It relieves customers of regulatory burdens while allowing omnichannel merchants to more easily offer a mix of eligible and ineligible products.

The Challenges of Traditional Substantiation Methods

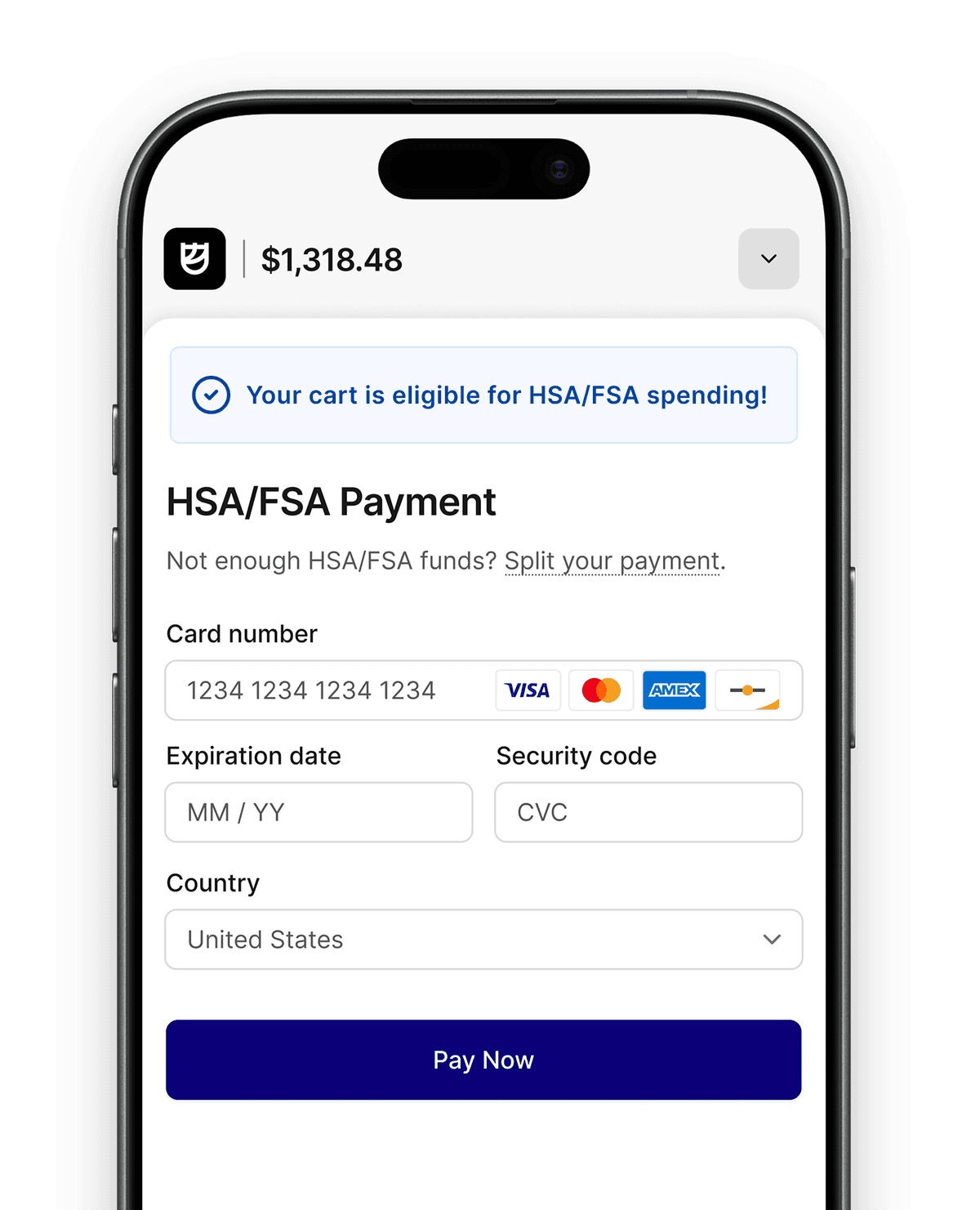

Without auto substantiation, the process of substantiating HSA/FSA purchases can be frustrating for both retailers and consumers. Customers have to distinguish between eligible and ineligible products when paying HSA/FSA funds, and then “split” their own carts accordingly. This process, simple with autosubstantiation, is confusing and unwieldy when done manually.

Furthermore, guidelines around eligibility are consistently evolving. For example, during the COVID-19 pandemic, IRS Announcement 2021-7 declared that personal protective equipment (PPE) is HSA/FSA eligible. Other proposed changes fail to make it into law, like a recent plan to extend eligibility to gym memberships and other fitness-related expenses. Amid this regulatory upheaval, consumers and retailers struggle to stay up to date on the HSA/FSA eligibility of different products and services.

Substantiating HSA/FSA purchases is especially challenging for retailers with diverse product inventories. Medical providers can rely on Medical Merchant Category Codes (MCCs) for simplified substantiation, but that option is unavailable to most retail brands.

IIAS: A Helpful (and Mandatory) Component of Auto Substantiation

An Inventory Information Approval System (IIAS) allows retailers to provide seamless auto substantiation for HSA/FSA purchases. Having such a system is also an IRS-mandated requirement for most retailers accepting HSA/FSA funds.

Pharmacies often avoid this mandate through the “90% rule,” which states that an IIAS is not required for business locations if at least 90% of the products sold in the previous tax year qualified as eligible medical expenses. However, most retailers fall well below that 90% threshold—making IIAS a legal requirement for HSA/FSA acceptance.

Breakdown: The IIAS Substantiation Process

IIAS systems instantly distinguish eligible from ineligible products at checkout, enabling split-cart transactions. For example, if a customer shopping at Scotty’s Supplements purchases a prenatal vitamin (eligible) alongside a t-shirt (ineligible), the IIAS system will automatically identify and process each product accordingly, requiring separate payment methods for each category.

Here’s a step-by-step look at how an IIAS system substantiates HSA/FSA purchases:

- The IIAS system collects information, including SKUs, about the products a customer adds to their shopping cart.

- The system compares the items to a list of eligible medical expenses according to IRS § 213(d).

- The system totals the eligible expenses.

- Eligible expenses are charged to the customer’s HSA/FSA account, while any ineligible expenses are charged to a separate payment method. (This is called a “split-tender transaction.”)

- The transaction information is either (a) sent immediately to the HSA/FSA administrator for substantiation or (b) stored according to recordkeeping requirements until a review is requested.

This automated process occurs in real time, providing seamless access to HSA/FSA funds for retailers and consumers while maintaining complete compliance with IRS regulations.

Technical Requirements for IIAS Integration

For an IIAS to be IRS-compliant, it has to meet some technical requirements:

- It must compare SKUs/UPCs to an IRS-approved list of § 213(d) eligible items.

- Transactions must be auto-substantiated in real time at the point of sale.

- Only eligible items can be approved for FSA/HRA purchases.

The retailer’s Point of Sale (POS) system must support an IIAS that meets these requirements.

Audit Risk & Compliance Management

In the rare event of an audit, the IRS’s primary focus is typically on the customer rather than the merchant. That said, retailers must provide precise transaction details for any HSA/FSA purchases. Without this documentation, the consumer can’t demonstrate the eligibility of their purchases, and the IRS may implement a 20% penalty (applied to the value of each purchase).

Retailers are required to maintain records for all HSA/FSA transactions for the sake of collaborating with potential IRS audits. These records should include:

- Purchase dates

- Product descriptions

- SKU-level eligibility confirmations

- Itemized receipts

- Documentation for any Letters of Medical Necessity

The ability to accurately maintain these records is one reason for retailers to partner with an HSA/FSA payment specialist.

Partnering With a Dedicated HSA/FSA Payment Provider

Retailers looking to maintain compliance while tapping customers’ tax-advantaged accounts should consider partnering with a dedicated HSA/FSA payment provider. These providers streamline the process of integrating an IIAS with a POS system, ensuring compliance along the way. For retailers, this provides both peace of mind and increased revenues.

How an HSA/FSA Payment Partner Improves CX

With the HSA/FSA payment processor integrated into the merchant’s checkout process, customers will be able to:

- See in real-time whether their purchases are HSA/FSA eligible or if they need a Letter of Medical Necessity (LMN).

- Acquire an LMN immediately (if needed) through an associated telehealth provider.

- Simultaneously purchase eligible and ineligible products at checkout (with HSA/FSA funds being applied only to the eligible purchases).

- Receive instant auto substantiation for eligible HSA/FSA purchases.

This friction-free experience boosts AOVs while encouraging brand loyalty.

The ROI of Using an HSA/FSA Payment Provider

When calculating the ROI of partnering with an HSA/FSA payment provider, retailers should factor in a variety of probable benefits:

- Larger cart sizes. Customers spend 30% more when they use their HSA/FSA card to make purchases.

- Increased customer retention. When surveyed, 92% of customers say they will return to shop with a retailer specifically because HSA/FSA funds were accepted.

- Enhanced customer relationships. Consumers appreciate the simplicity of having auto substantiation integrated into the checkout flow.

- Access to spending power. Americans hold a total of $150 billion in HSA and FSA accounts—a number that should grow as annual HSA/FSA contribution limits increase.

Checklist for Evaluating Your Ideal HSA/FSA Payment Partner

To maintain compliance and maximize ROI, retailers need to partner with the right HSA/FSA payment provider—one that consistently delivers reliable auto substantiation.

Here are some questions retailers should ask about each potential provider:

- Does the provider offer real-time, SKU-level eligibility verification?

- Does the provider support transactions involving Letters of Medical Necessity (LMNs)?

- Can the platform effectively handle mixed-cart transactions?

- How does the provider manage returns, refunds, and discounts?

- How flexible is the provider when adapting to inventory changes or adding new SKUs?

- Will the platform integrate seamlessly with your existing ecommerce and POS systems?

- What analytics and reporting capabilities does the provider offer?

If a HSA/FSA provider meets all of these standards, it should have a transformative effect on a retailer’s relationship with HSA/FSA account holders.

Customer Education & Experience

One of the main benefits of accepting HSA/FSA payments is the improved customer relationships. Businesses can further capitalize on this advantage by prioritizing education—using websites, social media accounts, and other channels to explain the nuances of HSA/FSA substantiation to customers.

Common Customer Questions Around HSA/FSA Purchases

HSAs and FSAs are confusing for account holders. Retailers can provide clarification by answering these common customer questions:

- “What products and services can I purchase with HSA/FSA funds?”

- “What documentation is required for reimbursement?”

- “How do I handle split transactions (when some products are eligible, and others aren’t)?”

- “What happens if I use my HSA/FSA for a non-eligible expense?”

By answering these questions in FAQ pages and other support resources, retailers become trusted partners for consumers. They also make it easier for people to use their HSA/FSA funds, which should increase average cart sizes.

Optimizing the User Experience

Consumers are often intimidated by the prospect of using HSA/FSA funds, a process that seems fraught with compliance risk and bureaucratic headaches. Retailers can alleviate customer stress by making the substantiation process as streamlined as possible.

This is another area where using a dedicated HSA/FSA payment partner proves advantageous. With the right system in place, retailers can offer digital tools for uploading recipes and tracking expenses.

Conclusion

For ecommerce brands and omnichannel retailers, accepting HSA/FSA payments unlocks serious business advatages—especially when a dedicated HSA/FSA payment provider streamlines the process.

Customers spend more when accessing tax-advantaged accounts, and they maintain loyalty for retailers who offer stress-free auto substantiation. Meanwhile, the retailers rest assured that they’re operating in compliance with IRS regulations.

In the midst of this opportunity, the next step for retailers is clear: Begin evaluating potential HSA/FSA payment providers. A successful partnership will bring larger AOVs, increased customer retention, and consistent legal compliance.